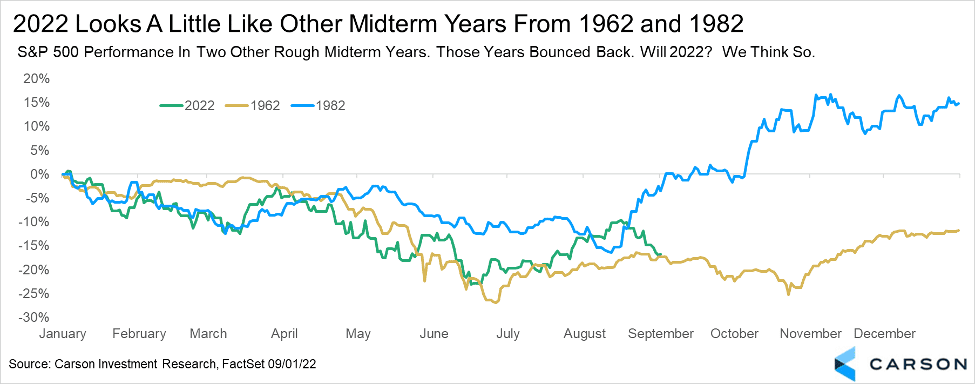

It continues to be a challenging year for stocks, but all is not lost. We believe there could be some decisive gains before year-end. Let’s look back at two other midterm years that were similar to 2022 in more ways than one.

- Historically, similar bad starts to midterm election years have been followed by stock market rallies late in the year.

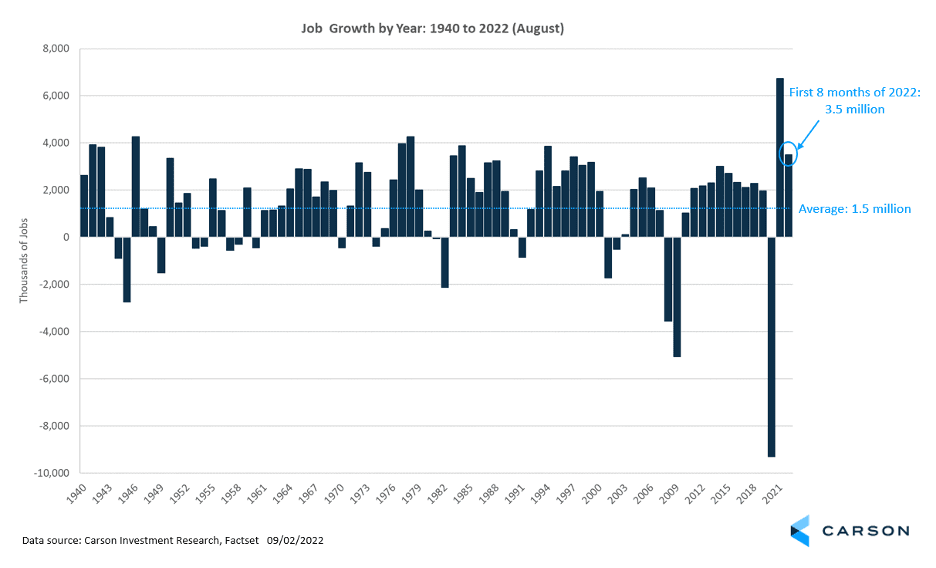

- More than 3.5 million jobs have been created over the first eight months of 2022, which is not typical of a recession.

- September is no doubt a volatile and historically weak month. So, buckle up.

- Supply chains are improving and gas prices are falling, signs that inflation has likely peaked in the U.S. Consumer confidence is also rising amid falling gas prices.

In 1962, first-term Democratic president John F. Kennedy faced a very tough midterm election, supply chain issues, Russia and the U.S. on the brink of war over a small island, Cuba (Taiwan today?), and a six-month 28% bear market without a recession. Sound familiar? Just for reference, the bear market this year corrected 24% in just more than five months. Stocks bottomed in late June 1962 but went on to nearly retest those lows during the Cuban missile crisis in late October. Stocks then soared 18% through the end of the year once the crisis calmed down.

In 1982, the market experienced historically high inflation, another midterm year, low consumer confidence, high gas prices, an aggressive Fed, an economy in a recession, and more challenges with Russia. This time stocks lost 27% in a 21-month bear market. At the lowest point, stocks were down more than 16% for the year in mid-August, but then one of the strongest rallies in stock market history took over. In about four months, stocks made up all the losses from the previous 21 months. What sparked it? It was all about inflation showing signs of peaking and rolling over.

Mark Twain said, “History doesn’t repeat itself, but it often rhymes.” Looking back at these two midterm years shows one key concept. We’ve had bad times before and stocks have bounced back. A lot of bad news is priced into the market right now, and should there be any good news on inflation, the war in Ukraine, the Fed, or the economy, there could be plenty of room for another late midterm-year rally in 2022.

A Positive Employment Report, In More Ways Than One

Good news did arrive last week in the form of the August employment report. This initially buoyed equities until news that Russia is cutting off gas supplies for Europe rocked markets late Friday — a reminder that global events can cause higher volatility over the short run.

The economy created 315,000 jobs in August. Since these numbers can be revised, it’s more useful to look at the average over the last three months — job growth averaged 378,000 each month between June and August. The bigger picture is the economy has created 3.5 million jobs this year, and there are five months left to go. Average annual job growth since 1940 is about 1.5 million; 2.3 million when recessions are excluded. This is a very strong labor market.

The August report also showed the unemployment rate rose from 3.5% to 3.7%. In his Jackson Hole speech last week, Fed Chair Jerome Powell said the Fed is focused on getting inflation down to its 2% target but that will involve bringing pain to households and businesses. So, are we starting to see signs of the pain Powell mentioned?

Not really. The unemployment rate is calculated by dividing the number of unemployed persons (those who are looking for a job) by the size of the labor force (employed + unemployed). In August, the ranks of unemployed increased but not because more people were laid off. It was because more people came back into the labor force and started looking for jobs. This is a good sign because it points to a more attractive labor market, certainly not something seen in a recession.

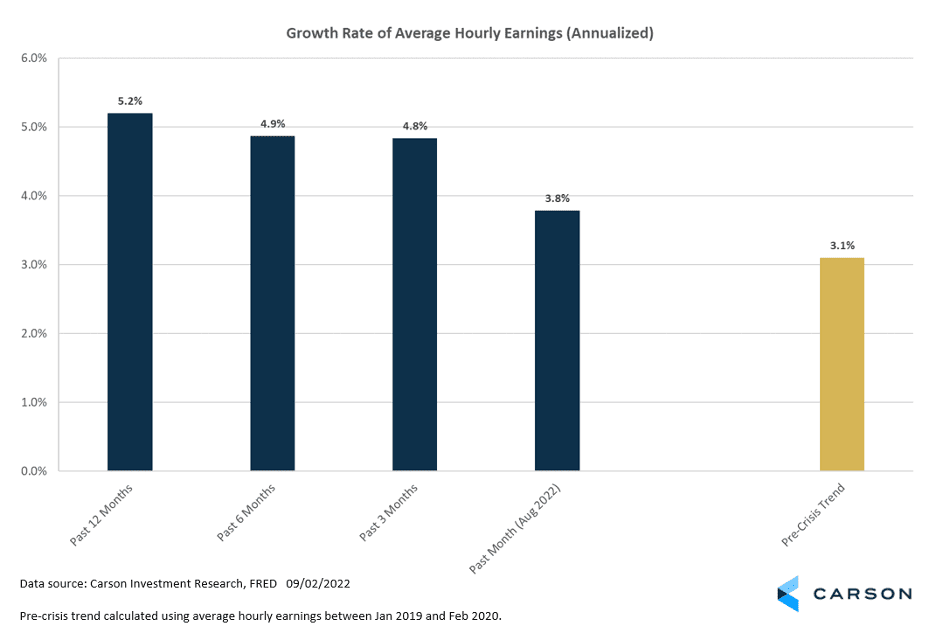

The connection between employment and prices is wage growth, at least as the Fed sees it. And there is good reason for this. Inflation can be impacted by several factors, including global oil, food prices, and supply-chain disruptions — as we’re all familiar with at this point. Stripping out the goods impacted by these sorts of factors leaves us with services inflation. This is what the Fed is really concerned about, and historically in the U.S., strong wage growth has led to higher services inflation.

But there was good news on this front, too. Average hourly earnings for private sector workers rose about 4% (at an annualized rate) in August, which is slower than the 5% rate it has averaged over the past year. It appears to be moving closer to the pre-crisis wage growth rate of about 3%.

Slower wage growth is not great news if you are employed, especially considering the high levels of inflation. Falling gas prices are providing some relief; but from the Fed’s perspective, the best news in the August payroll report was that wage growth slowed.

Many economists believe that for wage growth to slow, job openings have to fall — leading to slower employment gains and, ultimately, higher unemployment. So far, that’s not happening.

Wage growth has slowed despite job openings remaining extremely elevated. Job openings listed by employers are running twice as high as the number of unemployed workers. Before the pandemic the ratio was about 1.2:1, i.e., 12 jobs listed for every 10 unemployed workers. Now it’s 2:1. Employment gains slowed in August, but it was always unlikely that job growth would continue running at half a million a month. Moreover, layoffs remain at record lows. All this is exactly the opposite of what would be expected.

While it’s hard to pinpoint an exact reason, a significant factor may be that the economy is continuing to normalize after two years of massive pandemic-related shifts. The pandemic prompted workers to quit their jobs at a much higher rate. Some termed this the “Great Resignation,” but it was really the “Great Job Switch.” Workers did not quit their jobs to stop work. Instead, they quit to take another job — and, importantly, one with higher pay. Over the 12 months through July, “job switchers” saw wage gains of 6.7% on average, compared to 4.9% for “job stayers.”

As the economy normalizes, this trend is reversing. Quits have fallen 7% since November, with most of that decline occurring over the past four months. That may be why wage growth is falling without unemployment rising in a significant way.

That would be the ideal case for the Fed and the economy. If wage growth continues to fall, that is a good sign for the services part of inflation. It also means the Fed would not have to increase rates too much further. And if all that happens on the back of fewer quits as opposed to rising unemployment, that would indeed be the best case.

This newsletter was written and produced by CWM, LLC. Content in this material is for general information only and not intended to provide specific advice or recommendations for any individual. All performance referenced is historical and is no guarantee of future results. All indices are unmanaged and may not be invested into directly. The views stated in this letter are not necessarily the opinion of any other named entity and should not be construed directly or indirectly as an offer to buy or sell any securities mentioned herein. Due to volatility within the markets mentioned, opinions are subject to change without notice. Information is based on sources believed to be reliable; however, their accuracy or completeness cannot be guaranteed. Past performance does not guarantee future results.

S&P 500 INDEX

The Standard & Poor’s 500 Index is a capitalization-weighted index of 500 stocks designed to measure performance of the broad domestic economy through changes in the aggregate market value of 500 stocks representing all major industries.

MSCI ACWI INDEX

The MSCI ACWI captures large- and mid-cap representation across 23 developed markets (DM) and 23 emerging markets (EM) countries*. With 2,480 constituents, the index covers approximately 85% of the global investable equity opportunity set.

Compliance Case #01478809